What would you prefer: Rs 10,000 right now or Rs 10,000 five years from now?

Common sense tells us that we should take Rs 10,000 today because we know that there is a certain time value of money. The Rs 10,000 received now provides us with an opportunity to put it to work immediately and earn a certain return on it.

A single rupee today is worth more than a single rupee a few years down the line. Given this, households that have surplus funds in the form of savings want to invest those funds so that the value of the funds over the years does not go down.

There are various forms of investments at the disposal of individuals. These include real assets like a house, a car, a television, or financial assets like stocks in companies, bonds, units of funds, et cetera.

Traditionally, term deposits in banks, post office savings schemes, bonds and common stocks are the most accessible forms of investments available to the investors. Term deposits, post office savings schemes and bonds give a fixed return over a period of time.

Risk and Return

Investors would typically want to invest in an asset, which gives them maximum return on their investment. However, life is not as simple as that. Different assets come with different risk profiles.

Risk in a practical way can be defined as the chance that the expected outcome may not happen and the actual outcome may not be as good as the expected outcome.

For example, the risk of driving a vehicle too fast may lead the driver getting a speeding ticket or it might even lead to an accident. The New Oxford Dictionary of English defines risk as 'a situation involving exposure to danger.' Thus risk is always looked at in negative terms.

In case of investments the definition of risk is much broader. Risk in case of investment can be defined as the likelihood that the investor will receive a return on his investment that is different from the return he expects to make.

So risk not only includes bad outcomes when the returns are lower than what was expected, but it also includes good outcomes when returns are more than expected.

When investors are making an investment they expect to earn a certain return over the period the investment is made. But their actual returns may be different from the expected return and this is the source of risk.

For example, an investor invests a certain amount in a fixed deposit for a period of one year and expects a return of 5% (i.e. the interest on a one year fixed deposit that the bank gives is 5%). At the end of one year when the investment matures the investor will get a return 5%. So this is a risk less investment.

Instead of investing in the fixed deposit, the investor decides to invest the same amount of money in a particular stock. The investor having done his research expects say a return of 25% in one year's time (dividend and capital gains).

The actual return over this period might turn out to be greater than 25% or lesser. The company may not pay the dividend on time or the price of the stock may not rise as much as was expected. Herein he carries the risk. The actual return is not guaranteed.

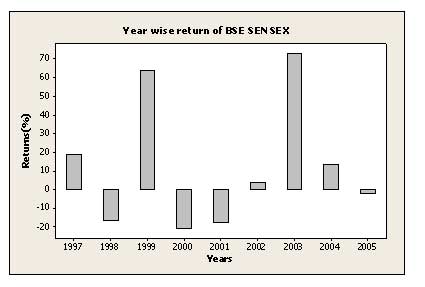

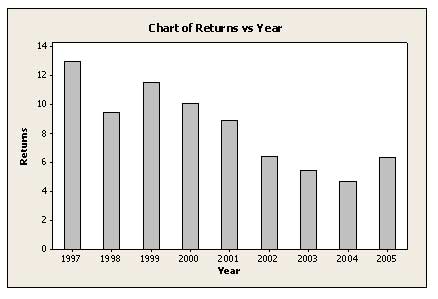

The figure 1 below shows the returns analysis of BSE Sensex over a period of 9 years, from 1997 to 2005. We can clearly see that the returns have varied from a negative 21% to positive 73% over these years. On the other hand, the returns on treasury bills (Treasury bills are securities with maturity period of less than or equal to one year. Issued by the government) just varied from about 13% to around 5% in 2004 (See figure 2).

Figure 1: Returns of BSE Sensex over 9 years

Source: The graph has been compiled from yearly closing price data on www.bseindia.com (The returns for 2005 is up to April 8th, 2005)

Figure 2: Returns of Government of India Treasury Bills over 9 years

Source: The graph has been compiled from the Bloomberg Data Terminal using Government of India Treasury Bills Index (The returns for 2005 is up to April 8th, 2005)

So, treasury bills give a fixed return over a period of time but common stocks do not. So, investors demand a premium from the common stocks for taking on extra risk.

In India, the investors on an average demand a premium of around 10.5% above the risk free rate. The risk free rate is generally taken to be the rate of return on treasury bills, as they are considered virtually risk free.

Common stocks are riskier because of various reasons. For one, the companies are not obligated to pay a dividend to the common stock holders, and secondly, in the case of liquidation, shareholders are the last to get paid after all the other security holders have been paid.

Thus the decision to invest in an asset with maximum return becomes difficult, as high returns come with high risk. The task of investment becomes formidable for the investors who must balance the returns from and risk involved in an asset.

Alternative investments

A major part of the household savings gets channeled into the so called traditional investments like fixed deposits (FDs), post office saving schemes, Public Provident Fund (PPF), etc.

But since the mid-90s interest rates have come down considerably and investments like FDs have been giving lesser return than the existing rate of inflation, or just a few basis points above the rate of inflation.

For example, the current inflation rate prevailing in India is around 5.1%, whereas the largest bank of India, the State Bank of India offers a return of 5.00% on deposits for more than 182 days but less than 1 year.

The rate for deposits of more than 1 year but less than 3 years is 5.5%. Another disadvantage with such forms of investment is that the lock in period is considerably high.

However, many other forms of investments are available to investors. Exchange traded funds, derivatives, real estate, gold, art, are just a few of the alternatives. With the spread of technology, investing in some of these alternative investments has become comparatively easier than before.

These investments are also good means of diversification. Diversification refers to the act of reducing risk by spreading the total investment across many different investments.

The idea of diversification is very old. It has even been mentioned by Shakespeare as early as the 16th century in his one of the most celebrated plays, The Merchant of Venice:

'My Ventures are not in one bottom trusted,

Nor to one place; nor is my whole estate

Upon the fortune of this present year;

Therefore, my merchandise makes me not sad.'

-- Antonio in Merchant of Venice, Act I, Scene 1

This shows that merchants did realise the importance of not putting all their eggs in one basket early on.

Conclusion

Diversification and investment in alternative forms of investments have become more important in recent times when the stock markets have proven to be more volatile and the government bonds are barely able to match the inflation rate.

Investors are looking to put their money in assets which give decent returns even if the stock markets are tumbling. For example, the value of a piece of art may rise if the inflation is on the rise irrespective of the performance of stock markets.

Similarly, gold does well in time of global tension. In this way, even if the investor loses money in the stock market, it is offset by the gains in his alternative investments.

A lot of these alternative investments have consistently given a higher return than the traditional investment securities.

For example, the real estate investments in the National Capital Region of Delhi have consistently provided a return of more than 10% over the last three years, in both the commercial and residential segments.

This is much more than the 5-6% return provided by government bonds and fixed deposits. At the same time, the returns are not as volatile as that witnessed in the stock markets.

But many of these investment types still remain a mystery to the investors. This is a first in a series of articles through which we hope to explain the nature of various forms of such alternative investments that are available to the investors.

Vivek Kaul is Research Scholar, ICFAI, and Nupur Hetamsaria is Visiting Research Scholar, Syracuse University, NY.

Disclaimer

While efforts have been made to ensure the accuracy of the information provided in the content, rediff.com or the author shall not be held responsible for any loss caused to any person whatsoever who accesses or uses or is supplied with the content (consisting of articles and information). Readers are advised to cross-verify the information and to also seek professional and expert advise before taking any decision based on the content provided above or acting on any recommendations made herein. The information or opinion provided herein is not a substitute for professional advice.