You might have read W. Somerset Maugham's classic short story, The Ant and the Grasshopper. In the story, Maugham, the master storyteller, turns the wisdom from an Aesop's Fable on its head.

The fable talked of how an ant that labours through the summer preparing for winter ends up a winner instead of the grasshopper who does nothing to prepare for the harsh months ahead. In Maugham's short story, Tom, the carefree but proverbial black sheep of his family, constantly gets into trouble only to be bailed out by his hardworking brother George.

Tom beats his brother's predictions of ending up in a gutter when he marries a rich lady, who, on death, leaves him a fortune, making him a winner and his brother a perpetually sulking loser. When it comes to real life, especially saving for the future, we all know that it is the fable's moral that works. The boring, but diligent, Georges triumph in the end.

How much should you save?

Whether you save regularly or irregularly, a question often comes visiting: "Am I saving enough?" Saving the right amount is crucial for at least two major reasons.

First, it is only when you save money that you can invest in options such as fixed deposits, public provident fund, stocks, mutual funds, real estate and gold to create a future income for meeting small and large requirements, such as the education and marriage of your children and your retirement.

Second, while it is necessary to prepare for the future, current needs also have to be taken care of. Equally important, we would like to have a life and enjoy it with our families.

Second, while it is necessary to prepare for the future, current needs also have to be taken care of. Equally important, we would like to have a life and enjoy it with our families.

But the problem is that beyond a point, the more you live it up, lesser are the chances of accumulating enough savings for a minimum decent standard of living in the future.

Clearly, drawing a balance between the present and future holds the key. The good news for you is that the balance is achievable if you follow certain rules that we present here.

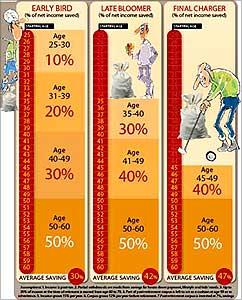

We, at Outlook Money, crunched numbers to give you an indicative idea of how three kinds of people -- those who start early, in their 20s (Early Birds), those who begin in their 30s (Late Bloomers), and finally, those who first reach for a piggybank in their 40s (Final Chargers) -- should save at various life stages.

The savings thumb rules

The Early Birds. When it comes to savings, the early birds have an advantage over those who are off the blocks late. They manage to save a decent pile for all their requirements with much lesser fuss. If you start saving from the age of 25, when you are likely to be in your first job, you can begin with saving 10 per cent of your net income (post-tax income) till the age of 30, by which time you are likely to be married.

If your savings horse proceeds even at a canter in this period, marked often by the absence of familial responsibilities, you will need lesser abstinence to save later, when responsibilities increase.

Step up your savings to 20 per cent in your 30s, 30 per cent in your 40s, and finally, to 50 per cent in your 50s. With this, you would have clocked a very healthy 30 per cent since age 25. Not a bad deal, is it?

Our assumptions for this as well as other categories are: income is net of taxes; partial withdrawals are made from savings for house down payment, education and marriage of children and for lifestyle needs; and average salary increments of 15 per cent take place.

Importantly, 30 per cent of the income at the time of retirement is earned in the 60s, after retirement, from jobs or assignments, and work life finally ceases at the age of 70, something already happening in urban India.

We have also assumed that the entire corpus is invested at 7 per cent and the surplus of the resulting income flow over current needs is reinvested in index funds that return 12 per cent a year.

Another assumption is that the corpus is liquidated at the rate of 6 per cent per annum starting from age 70. This gives a cushion if the person lives till the age of 90, or leaves an inheritance for the next generation.

The retirement money will be reinvested at 12 per cent per annum and will not be used fully till the expected life of 90 years. A portion of it will be left as a cushion, or for bequeathing.

Late Bloomers. Life is not rocket science. Circumstances might have prevented you from keeping your promise to yourself to start the savings journey early -- a super specialisation qualification that had to be completed, or a doctorate that took too much time, younger siblings who needed your support, or simply failure in meeting the right person to get married.

Such people need to start their savings vehicle in the second, if not the third gear. Assuming you start at age 35, you can begin this game of catch up by saving 30 per cent of your post-tax income till 40, zoom up to 40 per cent in your 40s and press the gas pedal further by saving 50 per cent in the 50s, till the chequered flag of the retirement finishing line looms up. You end up saving 42 per cent of your net income during the period.

Final Chargers. If you haven't been saving till age 45, you better hear the last and final call for the savings flight. Till age 50, you will have to jet at 40 per cent of your net income, followed by 50 per cent of net income in your 50s.

This will enable you to clock an average savings rate of 47 per cent, or almost half of what you get during this period.

Why you need to step up savings with age. The savings rates are higher for people who start saving later in life because the early risers get the benefit of compounding. This also spares them the agony of denying themselves in the present in order to provide for the future.

At the same time, you need to step up savings as you move on in life. At the beginning of your work life, you do well to even cover your expenses. At this point, a small but consistent amount of savings is crucial. Often, taking some practical steps is all it needs.

At the same time, you need to step up savings as you move on in life. At the beginning of your work life, you do well to even cover your expenses. At this point, a small but consistent amount of savings is crucial. Often, taking some practical steps is all it needs.

By the time you get married, your income has risen, but so have the costs, as you get down to setting up your own establishment, which, among other things, often involves taking loans for big-ticket items such as cars and consumer durables.

This stage typically lasts till your mid-30s or early 40s, after which your income simply pulls away from your expenses. The reason is that expenses don't grow as fast at this stage and, in many cases, the growth slows down. This is also the time when your savings should be the maximum and get invested.

In your 50s, you could have to bear big expenses such as higher education and marriage of children, besides relocation preparations for retirement. But the rise in your income with salary increments and investment income will let you continue saving.

You can also step on the gas when the big-ticket expenses get over and reinvest the residual savings.

Why saving enough is half the job done

You can save a lot and yet be forced to be miserly when you need money. This slip between the cup and the lip can happen if you haven't invested your savings in the appropriate order to give it the right opportunity to grow.

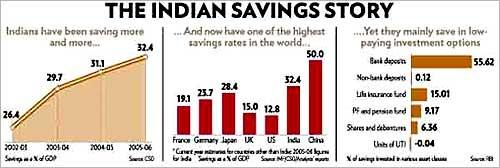

On an average, Indians are saving more, but the savings are getting invested in lower risk-lower return options such as FDs and mandatory retirement funds such as provident fund and life insurance. Some investments of this sort happen by default. Employees' Provident Fund is a case in point, where 12 per cent of your basic pay gets stashed away every month.

Besides, the risk averseness of many Indian investors, lack of awareness of options that bring higher returns, absence of quality financial advice and, sometimes, simply lethargy makes people invest money in their savings account in fixed deposits of the same bank.

This is despite the fact that equities have been found to be providing the best returns among all asset classes -- 18 per cent compounded annual growth rate (CAGR) since 1979. For instance, if Rs 1 lakh (100,,000) was invested in the Sensex, a PPF and a 5-year bank fixed deposit in 1982, today you would get Rs 55.12 lakh (5.512 million), Rs 7.69 lakh (769,000) and Rs 15.07 lakh (1.507 million), respectively.

Thumb rules for equity investing

Thumb rule No. 1: (100 minus your age). If equity is the best bet for brisk growth of our savings, then the logical question is how much should we invest in them either directly or via mutual funds?

The standard rule of thumb to determine your ideal equity exposure is a simple formula that suggests you subtract your age from 100. For example, if you are 35, then 100-35 or 65 per cent of your portfolio should be exposed to equity.

While this can be taken as an indicative formula, it would not, of course, be applicable to everybody at every point in their lives. For example, if you are a 30-year-old and part of a double income family with one young child, you could put in 70 per cent of your investments into the market.

However, if due to a sudden turn of events, you also have to provide for dependent parents and siblings, you should change your allocation and tweak down your equity exposure.

Thumb rule No. 2: Keep debt-equity proportion constant. If the age-based thumb rule does not apply to you, use a tactical allocation thumb rule. Here, you start off by investing, say, 60 per cent in equities and 40 per cent in debt, and continue keeping the ratio constant at all times.

If you find at the end of the year that equities have done well, you should trim your equity exposure in the next year, the assumption being that there is likelihood of a market downturn. However, in times of a long-running bull market, like the one we have been witnessing, this strategy may not be ideal.

Thumb rule No. 3: Factor in the trend. This thumb rule on trend-based asset allocation is the opposite of the previous one. The assumption in this one is that if the stockmarkets are going up, then that is the trend of the cycle, and you should enhance your equity exposure for the next year. Of course, trends could change and you might be trapped with a high equity exposure in a falling market.

How to follow the thumb rules. Since the thumb rules tend to contradict each other, you can adopt the following approach. Use the '100 minus age' formula if there is nothing exceptionally different in your profile and the assumptions fit you.

Keep that as the guiding number, and tweak it upwards or downwards depending on your specific circumstances. If you are in your mid-30s and single, you could invest more than 70 per cent in equities. If you are 60 and do not see yourself retiring for another eight years, you could invest more than 40 per cent.

How many mutual funds are enough?

Once you decide how much money you should place in equity, you need to figure out how much to keep in equity mutual funds and how much in stocks, if at all. Then, you will also have to figure out how many equity funds and stocks to buy.

The truth is that there is no magic number, though the number of funds in your portfolio should give you adequate diversification without making your returns suffer. Let's first examine mutual funds and then stocks.

How many mutual funds? You can target up to about 10 equity mutual funds. Apart from 10 being an easy number to track, academicians like J.L. Evans and S.H. Archer have shown in their research that most of the risk reduction due to diversification takes place in an aggregation of 8-10 securities.

Which categories of mutual funds? Typically, if you're venturing into equities for the first time, you can start with an exchange-traded fund (ETF). ETFs are low-cost cousins of index funds and invest in all the securities that lie in their benchmark index in the same proportion in which the index has them.

ETFs don't have risks associated with fund managers. They aim to give you returns in line with the market, so you don't lose or gain more than what the market does. Says Mumbai-based financial planner Jayant Pai: "It's not possible for active funds to outperform the market on a continuous basis. ETFs ensure that your returns are at least in line with the market." One ETF tracking a large-cap index like Nifty or Sensex should do fine.

Diversified equity funds. One ETF in your equity portfolio can be supplemented by a couple of diversified mutual funds, including equity-linked savings schemes. This will form the core of your portfolio and provide a baseline of expected growth.

As diversified equity funds invest in around 30-50 or in an even higher number of scrips, chances are the same scrip will feature in more than one fund if you have too many funds in your portfolio. Also, ensure that these schemes are different in styles. For instance, Franklin India Bluechip and SBI Bluechip are similar in objectives, so it does not make sense to have both in your portfolio.

Mid-cap funds and thematic funds. You can supplement your core funds with higher growth investment options. One of them is mid-cap funds. Though there are 26 mid-cap funds in the market, almost all of them target the same universe of stocks and there are negligible differences among them.

Then, there are thematic funds that invest according to a theme, such as infrastructure. You can invest in one mid-cap and one thematic fund.

How many stocks are enough?

After gaining equity experience through equity mutual funds, you can invest directly in stocks. Financial planners believe there isn't much merit in holding top-line equities as they would be anyway present in your mutual funds.

"Target some good, small companies that your funds may not have," says Pai. Although Nifty has 50 scrips and Sensex has 30 scrips, you don't need to hold as many, as tracking would be a problem then. Here, too, 10 sounds like a decent number. "Ensure that these 10 scrips are from different sectors," adds Pai.

Winning the savings game is about succeeding in providing for the future without losing out on your present. It is here that thumb rules serve as great guideposts. They show a happy middle path that lies between the ways of the ant and the grasshopper. In the end, you still win.

With reports from Pankaj Anup Toppo & Rajesh Kumar